Upwork (NASDAQ: UPWK) released its Q4 and full year 2025 earnings on February 9, 2026, and while the headlines boast record revenue and improved profitability, a closer look reveals several warning signs beneath the surface. Let's break down what the numbers actually tell us about the health of the world's largest freelancing platform.

Record Revenue Can't Hide Upwork's Growing Problems

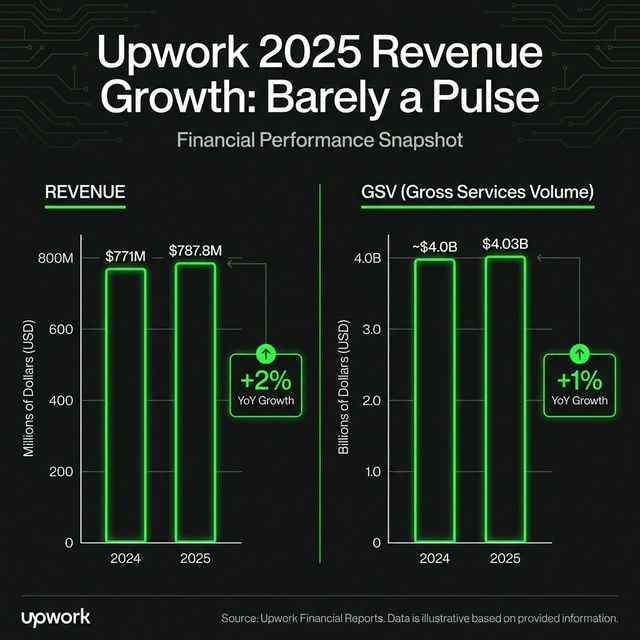

Upwork reported full-year 2025 revenue of $787.8 million, up just 2% year over year. Q4 revenue came in at $198.4 million, growing 4%. For a technology marketplace that positions itself at the center of the AI revolution, single-digit growth is underwhelming.

Gross Services Volume (GSV), the total value of work transacted on the platform, grew only 1% for the full year to $4.03 billion. That near-flat trajectory suggests the platform is struggling to expand the total pool of work flowing through it, even as management touts massive market opportunity.

Upwork Is Losing Clients — And That's a Big Problem

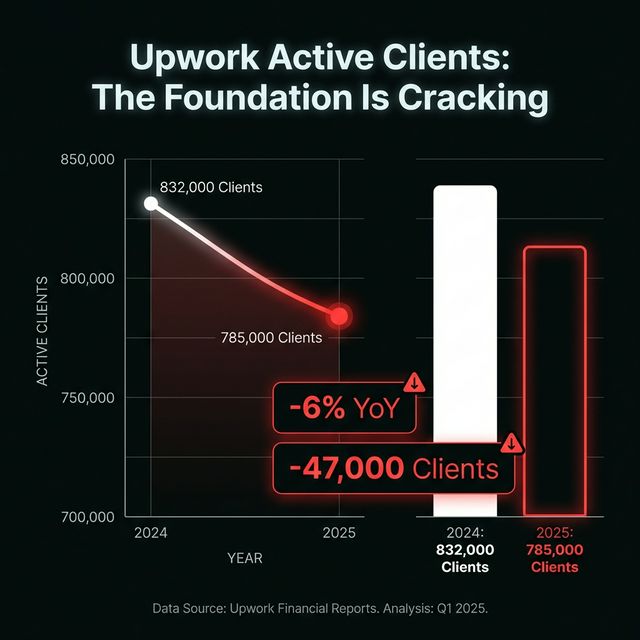

Perhaps the most concerning data point in the entire report is the decline in active clients. Upwork ended 2025 with 785,000 active clients, down 6% from 832,000 a year earlier. That's a loss of roughly 47,000 clients in a single year.

For a marketplace business, the client base is the foundation everything else is built on. Upwork is partially offsetting this loss by extracting more value per client — GSV per active client rose 7% to $5,129 in Q4. But relying on fewer clients spending more is a fragile growth model. It raises a critical question: is the platform retaining its best customers while shedding smaller ones, or is it broadly becoming less attractive?

Enterprise Revenue Is Shrinking, Not Growing

Upwork's enterprise segment, which was supposed to be a major growth engine, posted a 3% revenue decline in Q4 and a 2% decline for the full year, dropping from $107.2 million to $104.9 million. This is the segment where Upwork launched its Lifted subsidiary in August 2025, acquired Bubty and Ascen, and invested heavily in go-to-market strategy.

So far, that investment has not translated into top-line growth. Management noted they won two new Lifted clients in Q4, but for a business unit generating over $100 million in annual revenue, that pace of new client acquisition is modest at best.

The GAAP Earnings Drop Looks Alarming

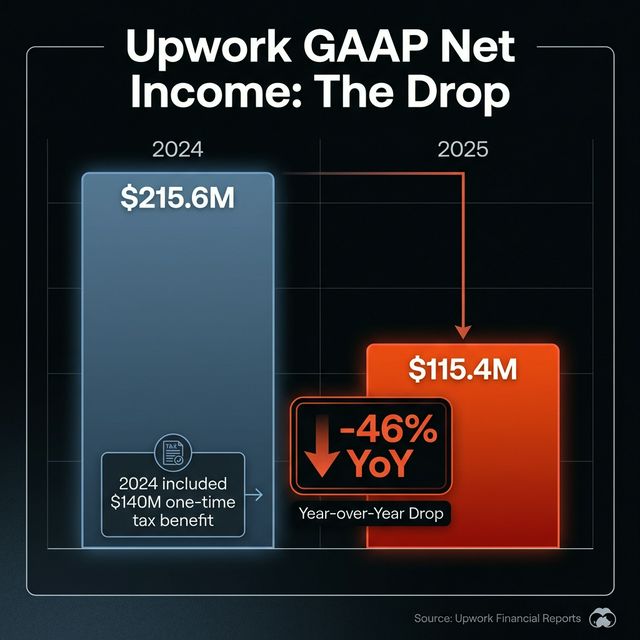

Full-year GAAP net income fell 46% from $215.6 million to $115.4 million. Diluted EPS dropped from $1.52 to $0.84. On the surface, that looks like a company in decline.

Context matters here: the 2024 figures were inflated by a one-time, non-cash tax benefit of $140.3 million from releasing a valuation allowance on deferred tax assets. Stripping out that anomaly, underlying earnings actually improved. But investors scanning headlines will see a company whose reported profits nearly halved, and perception matters in the market.

Debt Maturity Is Approaching

A detail that deserves attention on the balance sheet: Upwork reclassified $359.8 million in debt from noncurrent to current liabilities. This means the debt is maturing within the next twelve months and will need to be refinanced, repaid, or otherwise addressed. While Upwork has $294 million in cash and $378 million in marketable securities, managing this maturity will be a near-term priority that could limit financial flexibility.

The Bright Spots: Profitability and AI Momentum

It's not all bad news. Upwork made genuine progress on profitability and operational efficiency in 2025.

- Adjusted EBITDA grew 35% to $225.6 million, with margins expanding from 22% to 29%.

- Free cash flow surged 60% to $223.1 million.

- Total operating expenses declined 9% while revenue grew.

Upwork's AI narrative also shows real traction. GSV from AI-related work surpassed $300 million on an annualized basis, up over 50% year over year. AI integration and automation work specifically grew more than 90%. These are legitimately strong growth numbers in a category that should continue expanding.

The Business Plus offering for SMBs showed encouraging early momentum as well, with GSV up 24% quarter over quarter and active clients growing 49% quarter over quarter in Q4.

2026 Guidance: Acceleration Promised, Not Yet Proven

Management guided for 6% to 8% revenue growth in 2026, targeting $835 million to $850 million. Adjusted EBITDA guidance of $240 million to $250 million implies continued margin expansion. GSV is expected to grow 4% to 6%.

That would represent a meaningful acceleration from 2025, but it remains to be seen whether Upwork can deliver. Q1 2026 revenue guidance of $192 million to $197 million implies a typical seasonal dip, not an immediate inflection.

What This Means for Freelancers and Businesses on Upwork

For freelancers, the shrinking client base is the number to watch. Fewer clients on the platform means potentially fewer opportunities, though rising spend per client could mean larger and more valuable projects for those who remain active.

For businesses using Upwork, the platform's heavy investment in AI tools and the Uma AI assistant could improve the experience of finding and managing talent. The OpenAI partnership for AI training and certifications may also raise the quality bar for available freelancers.

The Bottom Line

Upwork is becoming a leaner, more profitable company. But profitability improvements driven primarily by cost-cutting rather than revenue growth have a ceiling. The declining client base, stagnant GSV, and shrinking enterprise revenue are structural concerns that efficiency gains alone cannot solve.

The bull case depends on AI-driven work, the SMB Business Plus product, and the Lifted enterprise initiative converting into sustained top-line acceleration in 2026 and beyond. The red flags in this report don't signal a company in crisis, but they do suggest one that needs to prove its growth story is real — and soon.

Disclaimer: This article is for informational purposes only and does not constitute financial or investment advice. Always conduct your own research before making investment decisions.

Want to boost your Upwork success?

Don't rely on platform trends alone. Optimize your profile to win more clients regardless of market conditions.

Polish My Profile